The center of aluminum scrap prices fluctuated upward around the National Day holiday. As of October 9, the SMM A00 aluminum price closed at 20,960 yuan/mt, up 190 yuan/mt from September 25. Ahead of the holiday, enterprises in Henan, Jiangxi, Shandong, and other regions actively stockpiled, driving up prices for some varieties. On the first trading day after the holiday, the aluminum scrap market followed the overall upward trend, supported by a sharp rise in spot primary aluminum, with mainstream varieties such as baled UBC and shredded aluminum tense scrap generally increasing by 100 yuan/mt. Regional performance varied significantly: the Yangtze River Delta region actively followed the rise, while key secondary aluminum hubs adjusted prices more cautiously.

Divergent views emerged regarding the subsequent trend of aluminum scrap prices. Some participants in the secondary aluminum industry believe that after the National Day holiday, aluminum scrap prices will maintain a strong, fluctuating pattern, as the tight supply fundamentals are unlikely to ease in the short term, providing solid support for prices. They expect aluminum scrap prices to strengthen in October, guided by primary aluminum prices. However, other feedback suggests that while downstream demand remains stable with a positive outlook, scrap utilization enterprises' acceptance of high-priced raw materials and their tendency to drive down prices may still limit the upside. Based on SMM's comprehensive assessment, the overall aluminum scrap market is expected to hold up well in October, with the mainstream price range for shredded aluminum tense scrap (including moisture) projected to hover around 17,500–18,000 yuan/mt. Market attention should focus on the sustainability of post-holiday downstream demand and further guidance from primary aluminum price movements.

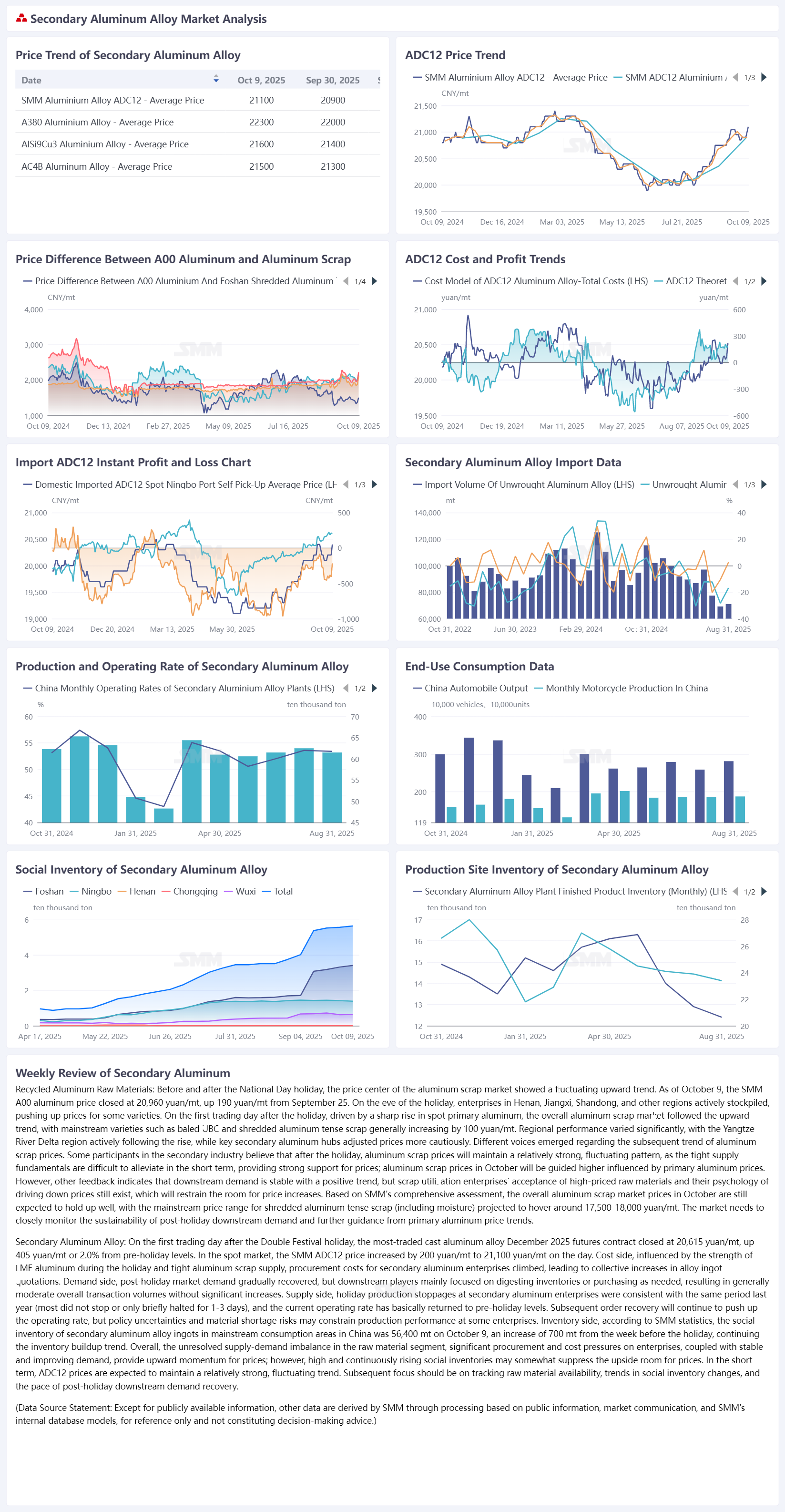

On the first trading day after the holiday, the most-traded cast aluminum alloy futures contract 2512 closed at 20,615 yuan/mt, up 405 yuan/mt or 2.0% from the pre-holiday level. In the spot market, the SMM ADC12 price rose by 200 yuan/mt to 21,100 yuan/mt on the day. Cost side, influenced by the strength of LME aluminum during the holiday and tight supply of aluminum scrap, procurement costs for secondary aluminum enterprises climbed, driving collective price increases for alloy ingots. Demand side, post-holiday market demand gradually recovered, but downstream buyers continued to digest inventories or purchase as needed, resulting in generally moderate transactions without significant volume growth. Supply side, holiday production halts at secondary aluminum enterprises were consistent with the same period last year (most did not suspend operations or only briefly halted for 1–3 days), and the current operating rate has largely returned to pre-holiday levels. Subsequent order recovery is expected to further push up operating rates, but policy uncertainties and material shortage risks may constrain production performance at some enterprises. Inventory side, according to SMM statistics, social inventory of secondary aluminum alloy ingots in mainstream consumption areas stood at 56,400 mt on October 9, an increase of 700 mt from the previous week before the holiday, continuing the inventory buildup trend. Overall, persistent supply-demand imbalance in raw materials, coupled with significant procurement and cost pressures on enterprises and steadily improving demand, provides upward momentum for prices; however, high and rising social inventories may impose some constraints on upside room. In the short term, ADC12 prices are expected to hold up well, with close monitoring needed on raw material availability, trends in social inventory changes, and the pace of post-holiday downstream demand recovery.